Most people who buy annuities think they’re choosing a calm, steady path for their money. Something safe. Something predictable. Something that won’t shift under their feet. But once you dig into how annuities actually work, you find a different story hiding behind the glossy charts and smooth sales talk. Currency shifts, foreign exchange rules, and tax traps can quietly eat into your returns, and most people never see them coming. These hidden costs don’t show up in bold letters. They don’t get explained in simple words. And they almost never get discussed at the moment you’re deciding what to do with your savings.

How Currency Risk Quietly Shapes the Real Value of Your Annuity

Before any founder or business owner commits money to an annuity, it helps to understand how currency movements can change the real value of every dollar you put in.

Many people treat annuities like a sealed box that stays steady no matter what happens outside. But the truth is simpler and more uncomfortable.

When your annuity involves a foreign currency at any point in its life cycle, the value of your future payouts rises and falls with every shift in the global market.

You may never see these shifts happening, but they shape the real return you get, the timing of your cash flow, and the total amount you can actually use in your business.

How Foreign Currencies Sneak into Ordinary Annuities

Even when you think you are working with a domestic product, your annuity might rely on foreign assets. Insurance companies often buy international bonds or use overseas investment vehicles to support the payout structure.

You may receive your income in dollars, but the underlying value is tied to things you never see.

When those foreign currencies strengthen, your annuity may quietly gain value. When they weaken, your long-term return can slowly drain away without a single warning.

Why Currency Volatility Can Outrun Your Planning

Business owners often assume they can plan their cash needs down to the quarter or even the month. Currency markets do not play by those rules. They move around the clock and react to elections, trade policy, war, inflation, and central bank decisions happening thousands of miles away.

Your annuity may be built on a twenty-year timeline, but currency swings can happen overnight. This creates friction when you are counting on a fixed payout to fund hiring, product development, or expansion.

What looks stable on paper may vary in real spending power by the time it hits your bank account.

How Long-Term Plans Get Distorted by Short-Term Shocks

Many founders choose annuities because they want smooth income in the future. But currency shocks do not wait for your schedule. A sudden change in a major currency can shift the real buying power of your payout for years.

Even when markets settle, the damage is already done. This makes long-term planning harder, especially for businesses that rely on steady cash to run experiments, fuel growth, or handle predictable burn.

The Hidden Spread Between What You Expect and What You Get

There is always a difference between the currency rate you see online and the rate used deep inside an annuity contract. Companies often price in buffers that protect them but reduce the real value of your investment.

This spread is rarely explained in simple words, but it affects how much your money can actually do for you years later. When founders plan for future capital needs, this gap can create underfunded plans and delayed milestones.

Why Global Interest Rates Make Currency Risk Even Bigger

Interest rates in other countries shape the value of their currencies. When rates shift, the currency often shifts too, and your annuity feels the change whether you realize it or not.

If the country where the annuity’s underlying assets sit cuts rates, the currency may weaken, and your future payout loses strength.

If they raise rates, the currency might strengthen, but it may also push the insurance company to adjust its own internal returns. Nothing moves in isolation, which is why founders need to watch more than just their home economy.

How Businesses Using Annuities for Stability Can Still Face Instability

Many business owners use annuities to create predictable cash flow during slower years. But currency exposure can make that flow feel less steady than expected.

The amount you planned to use for payroll or equipment may not stretch as far when exchange rates shift.

This creates tension between the need for stability and the reality of global financial movement. The more your business depends on long-term predictability, the more currency risk can work against you.

How Currency Risk Compounds Over Long Holding Periods

A small currency shift in one year may not seem like a problem. But annuities compound these small shifts over long periods. When the currency tied to your annuity stays weak for a few years in a row, the effect becomes much bigger and harder to reverse.

This creates a long-term drag on the value of your money, even if everything else in your business goes right.

Founders who expect a stable financial runway in the future may discover a runway that is shorter, thinner, and more unpredictable.

Why Many People Never See Currency Risk Coming

Currency exposure is rarely presented upfront. It hides behind the product’s surface, behind smooth charts and simple words like fixed, guaranteed, or stable.

Most buyers assume that these words mean their payout will stay the same in real value, even though currency markets do not respect those assumptions. This lack of clarity creates a false sense of safety that can hit hard later when expenses rise but your payout does not.

How to Protect Your Business From Currency-Driven Surprises

To avoid being blindsided, founders need more visibility into how their annuity is structured.

This means understanding what currencies the underlying assets are tied to, how payouts will be converted back into your local currency, and whether the company builds in buffers that reduce your final return.

When you understand these parts clearly, you can match the annuity to your real needs instead of crossing your fingers and hoping nothing shifts. This gives you more control over future capital, which is crucial when growth depends on timing.

Why Tracking Currency Trends Helps You Plan Better

You do not need to become a currency trader, but keeping a simple eye on major global currencies gives you a sense of how your annuity might behave in the long run.

When you watch these movements, you gain an early signal of whether your payout may deliver more or less buying power in the future. This lets you adjust hiring plans, expansion plans, or savings strategies before the impact hits your business.

The Simple Rule for Making Currency Risk Work in Your Favor

Businesses grow stronger when decisions are based on clear understanding rather than hope.

Currency risk becomes far less threatening when you choose annuity structures that match your economic reality, not just the marketing promise.

When you ask sharper questions, review the underlying currency exposure, and avoid products that depend on unstable markets, you reduce the chance of a painful surprise.

And when you build your financial strategy on steady ground, you unlock more freedom to build, innovate, and move fast.

The Hidden FX Fees Nobody Talks About but Everyone Pays

Before a founder commits a single dollar to an annuity that touches another currency, it helps to know that foreign exchange fees are baked into almost every step of the process. These fees rarely appear in bold print or plain language.

They hide inside conversion rates, administrative costs, and internal pricing structures. They also flow through your payouts in ways that slowly shrink the real power of your money.

What makes FX fees so dangerous is not just their size but their quiet presence. They show up whether markets move up or down, whether your annuity grows or stalls, and whether you ever knew they existed in the first place.

Why FX Fees Hide Inside Everyday Conversions

Any time your money leaves one currency and enters another, a fee appears. It may be small, but it is always there. When you buy an annuity tied to foreign assets, the company needs to convert your dollars into the currency used for the underlying investments.

That conversion gives the company an opportunity to embed a spread, which is a gap between the real rate and the rate you receive. You do not notice it because it is built into the math, not added as a line item.

Over the life of an annuity, this gap adds up. What starts as a small cost at the entry point can become a long-term drain that slowly eats into every future payout.

How FX Spreads Change What You Think You Are Earning

Many founders look at the stated return of an annuity and assume that number reflects reality. But FX spreads can change the flow of money so much that the real return becomes something very different.

The stated rate may look stable, but the amount that arrives in your account may feel smaller than expected once conversion costs take their share.

This is especially common in cross-border annuities or products tied to international assets. The more conversions involved, the more spread gets embedded into the final number.

How FX Fees Multiply During Payout Cycles

Annuities often involve multiple conversions over time. Money moves into the foreign currency when you purchase the product. It may move again inside the fund as the company rebalances. Then it moves once more when your payout is sent back to your home currency.

Each conversion introduces another slice of cost. These slices are not obvious unless you know to look for them. For founders who expect predictable income, these repeated conversions create unexpected volatility.

You might expect your payout to fund a product launch or a hiring round, only to realize that FX costs trimmed the amount below what you planned for.

Why FX Costs Matter More in Low-Return Environments

When markets deliver high returns, FX fees may feel like background noise. But when returns are modest, the fees take a bigger bite. If an annuity offers a conservative rate, even a small spread can meaningfully reduce your gains over time.

This matters for founders who use annuities as a safe complement to higher-risk investments.

You may think you are buying stability, but FX friction can reduce the very safety you sought by making the growth path thinner than expected.

Why Fees Expand During Market Stress

Currency markets behave differently during stress. When volatility rises, spreads tend to widen. This means the cost of converting money gets bigger right when you need stability the most.

If you depend on future payouts during a tough economic cycle, FX stress can make those payouts weaker.

Founders facing rising burn rates or unexpected costs may feel the pressure even more when their annuity produces less real buying power than planned.

How FX Costs Create an Invisible Tax on Your Money

Every fee inside a currency conversion acts like a hidden tax. It reduces the amount that actually enters your account. Unlike normal taxes, you do not see a form, a line item, or a clear explanation.

You only see a smaller number. Over long periods, this hidden tax can reshape your entire financial plan. It reduces the capital you expect to reinvest into your business.

It delays your ability to scale. It changes what you can afford in the future. And it does all of this quietly, without you ever approving it.

Why Many FX Fees Are Impossible to Challenge

With most financial products, you can negotiate or shop around for better rates. FX spreads inside annuities do not work that way. They are often baked into the contract and not disclosed in simple terms.

Even if you find the spread mentioned somewhere, it is usually buried deep in legal language. This means you cannot push back or negotiate. You must accept whatever structure the company built.

This lack of clarity gives the provider complete control over a cost that directly affects the strength of your long-term financial plan.

How FX Fees Affect Global Teams and Cross-Border Businesses

Many startups today work across borders. They hire talent abroad, sell in multiple countries, and rely on complex cash flows. Annuities that involve FX exposure can clash with these realities.

If your business needs reliable cash in dollars, euros, or another currency, a poorly structured annuity can disrupt your planning rhythm. Even a few unexpected conversion costs can alter your monthly runway.

This is especially risky for companies operating in tight markets where every dollar counts.

Why FX Risk and FX Fees Are Not the Same Thing

It helps to understand that FX fees are different from FX volatility. Volatility changes your return based on market movement. Fees reduce your return no matter what the market does.

This means you face two separate drains. One comes from unpredictable price swings. The other comes from predictable but hidden costs.

You cannot control volatility, but you can control whether you choose a product where fees quietly chip away at your long-term value. Once you see the difference, you gain power over decisions that shape your financial future.

How to Reduce FX Drag Without Abandoning Annuities

Founders do not need to avoid annuities entirely. They simply need to understand where FX exposure lives inside the product. You can choose annuities tied to your local currency.

You can ask clear questions about conversion points and spreads. You can avoid products that involve multiple layers of foreign assets.

And you can use annuities as part of a larger plan instead of trusting them as your primary foundation. When you reduce FX drag, you protect more capital for your business, your growth plans, and your long-term stability.

Why Clarity on FX Structure Gives You a Strategic Advantage

When you understand FX mechanics, you move from feeling blind to feeling in control. This control lets you align your annuity decisions with your real business needs rather than relying on assumptions. You gain sharper timing. You gain cleaner planning.

You gain more predictable returns. And most importantly, you keep more of your money working for your business instead of losing it to invisible conversions.

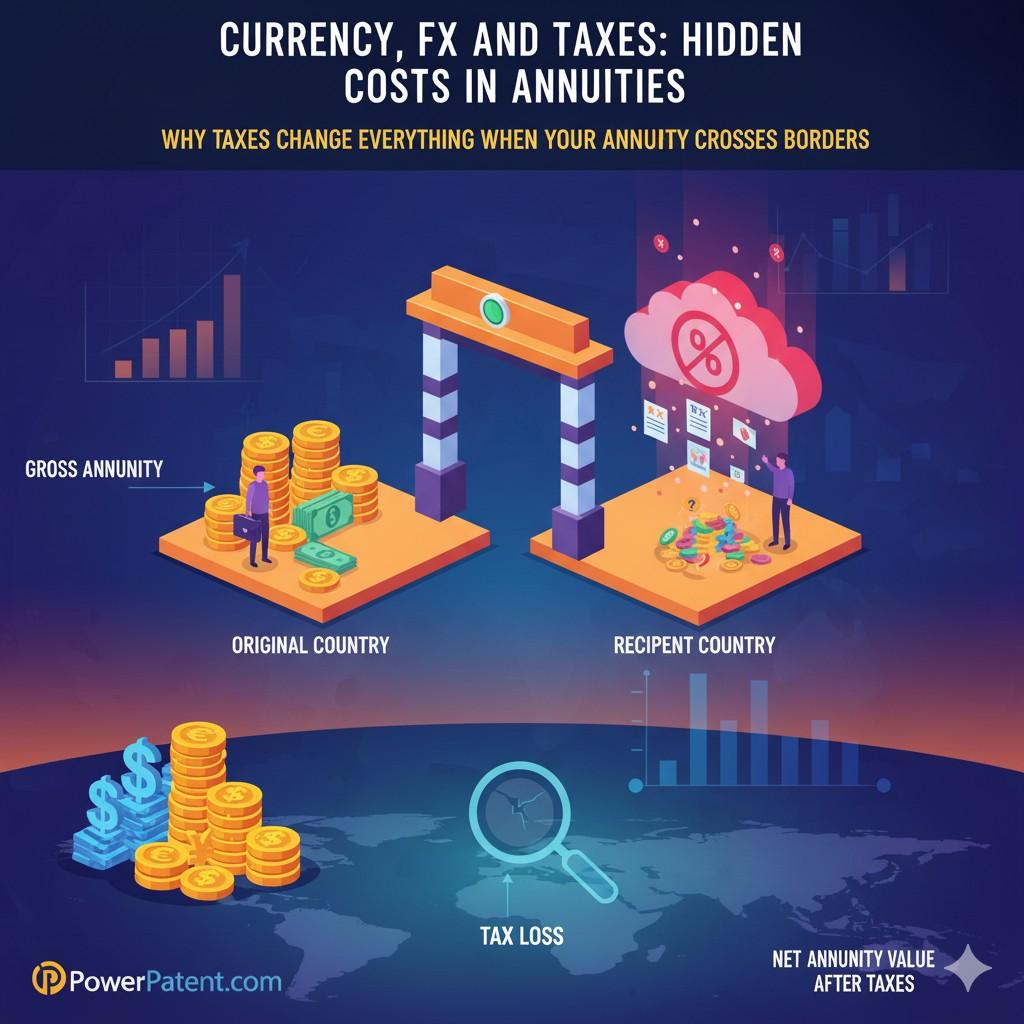

Why Taxes Change Everything When Your Annuity Crosses Borders

Before any founder treats an annuity as a safe long-term plan, it helps to understand how taxes can change the true value of every payout. Taxes are not a simple line item in cross-border annuities.

They shape the contract, the timing, the payout schedule, the real return, and the amount you actually keep. Even when an annuity looks clean and predictable, tax rules can twist the outcome in ways that feel unfair and completely unexpected.

The challenge is that cross-border tax rules rarely move in straight lines. They shift with local laws, international treaties, reporting requirements, and the way each country defines income.

All these moving pieces can turn what looks like a safe plan into a slow-moving financial trap if you do not understand the hidden details.

How Tax Rules Differ Across Countries

Tax systems do not match from place to place. One country may treat annuity income as ordinary income.

Another may treat it as investment income. A third may apply withholding taxes before the money even reaches you. These differences matter because they decide how much of your annuity survives.

A payout that looks strong on paper may shrink once foreign tax authorities take their share. This becomes even more complicated when both countries try to tax the same income.

Even if there is a treaty in place, the rules may not eliminate the burden entirely.

For founders who expect a clean and simple plan, these layered rules can create friction that slows down financial plans and reduces the amount of money available for growth.

Why Withholding Taxes Quietly Drain Your Payout

When an annuity crosses borders, withholding taxes can appear before you ever receive the money. These tax deductions happen at the source, meaning the insurance company or foreign government takes a portion before sending the rest to you.

This is not always obvious in the contract. It often shows up as a smaller payout without explanation.

Many founders assume the lower number is due to market changes or FX movement, when in reality the tax authority claimed its share. Once this money is taken, it is often difficult or slow to recover.

The paperwork alone can stretch for months, which creates timing problems when you are planning for predictable cash flow inside your business.

How Double Taxation Happens Without Warning

Even when countries have tax treaties, double taxation can still occur. You may pay withholding taxes abroad and then owe taxes again in your home country.

You may be eligible for a credit, but the credit may not cover the full amount. The system is not built to protect you. It is built to apply rules as written, which sometimes leaves gaps that cost you real money.

For founders who assume an annuity offers a stable, tax-efficient way to secure future income, double taxation can feel like a trapdoor opening under their feet.

This reduces capital for hiring, expansion, and product development, and it often appears at the worst possible time.

Why Tax Timing Matters More Than Most People Realize

Taxes do not only affect how much money you receive. They also affect when you receive it. If your annuity payout is delayed by reporting requirements or foreign tax filings, your business may lose momentum.

Cash you planned to use for a marketing push or new equipment may arrive months later. Timing is everything for startups, and tax delays can disrupt your entire planning rhythm.

Even a small delay can ripple through hiring cycles, vendor payments, and runway calculations. This is why founders need to see taxes not as a static cost but as a force that shapes the entire flow of money.

How Tax Definitions Change the Real Nature of Your Income

Countries define income differently. Some tax the portion that represents growth. Some tax the full payout. Some divide your annuity into a return-of-capital portion and a taxable portion.

If you do not understand how your home country treats annuity income, you may assume you owe less than you actually do. This misunderstanding creates surprise liabilities.

For founders who already juggle payroll, compliance, and growth planning, an unexpected tax bill can drain confidence and force sudden adjustments.

When you treat taxes as part of the structure, not just an add-on, you avoid these surprises and build a more stable plan.

Why Currency and Taxes Work Together in Ways Most People Miss

Tax authorities usually convert your payout into your home currency before calculating what you owe. If the conversion happens during a bad FX window, you might owe more tax on money that effectively lost value in real terms.

This creates a situation where you pay tax on income you never truly received. Currency can amplify tax pain in ways that feel completely disconnected from your actual financial experience.

For founders trying to manage runway and growth, this mismatch can take away funds that were meant to move the business forward.

How Changing Tax Laws Can Reshape Your Long-Term Plan

Tax laws do not stay still. They evolve with politics, economic pressure, and shifting priorities. A cross-border annuity that seems efficient today may become expensive later. If your payout period lasts ten or twenty years, law changes can happen multiple times.

Some changes come with transition windows. Others take effect immediately. Either way, the shape of your financial future may shift without warning.

This is why founders need flexible plans that adapt to tax change, rather than locking themselves into structures that only work under old rules.

Why Business Owners Need Transparent Tax Reporting

If your annuity crosses borders, reporting becomes more complicated. You may need foreign income declarations, residency documents, proof of withholding, or compliance statements.

These requirements are not optional. Missing a document can delay your payout or trigger penalties.

Many founders underestimate the time and energy this takes. In some cases, tax compliance becomes a project of its own, distracting you from product development and customer growth.

Clear reporting is not just about staying legal. It is about keeping your financial engine running without disruption.

How Tax Inefficiency Reduces Your Strategic Freedom

Every dollar lost to unexpected taxes is a dollar you cannot use to hire someone, enter a new market, or build a new feature. Tax inefficiency is not just a cost. It is a limitation.

It puts your future opportunities on a smaller and narrower track. Founders thrive when they have the freedom to adapt, but unexpected tax burdens make that freedom more expensive.

When an annuity reduces your flexibility, it affects more than your balance sheet. It affects your speed, creativity, and ability to move ahead of competitors.

How to Build a Tax-Aware Annuity Strategy Without Losing Momentum

Founders do not need to become tax experts. They simply need to understand the basic shape of the tax landscape.

When you ask clear questions, review tax exposure up front, and understand how both countries treat your income, you create a plan that protects your future buying power. You avoid the shock of double taxation.

You reduce reporting friction. You keep more money working inside your business, where it fuels growth. This approach turns taxes from a surprise into a known variable, which is exactly the kind of clarity every founder needs.

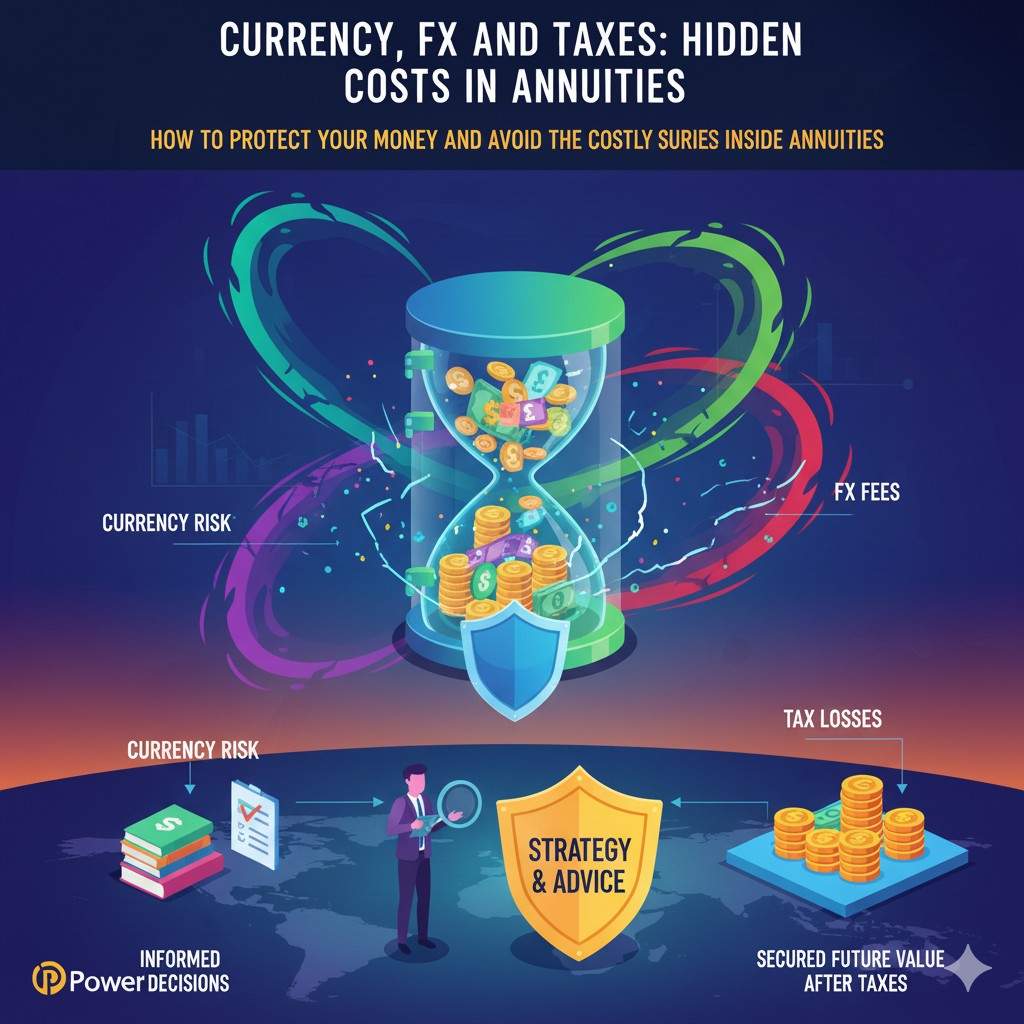

How to Protect Your Money and Avoid the Costly Surprises Inside Annuities

Before a founder signs any annuity contract, it helps to slow down and look at what protection really means in this context. Protection is not about choosing the product that claims to be safe. Protection is about understanding how the moving parts inside the product affect your real-world outcomes.

Currency shifts, FX spreads, and tax layers can turn a quiet long-term plan into a financial maze if you do not see them early.

What you want is not only stability but control. You want predictable access to capital when your business needs it most. You want clarity instead of guesswork.

You want to protect the future of your company, not bind it to a system that reduces your flexibility.

Once you understand how these hidden forces operate, you can build a plan that keeps your money working for you instead of slipping away in places you never noticed.

How Clarity at the Start Prevents Pain at the End

Many people approach annuities the same way they approach insurance forms. They trust the headline message and assume the fine print does not change the big picture.

But annuities tied to currency movement, FX conversion, and foreign taxes do not play by simple rules. If you do not ask sharp questions at the beginning, you inherit problems later. The early stage is where you get your leverage.

This is where you figure out how much of your investment is exposed to foreign markets, how many conversions will happen, and how each conversion changes your return.

When you gain clarity early, you block surprises later. For founders who need predictable capital to keep moving fast, this clarity is priceless.

Why Understanding the Real Structure of the Annuity Gives You Power

The structure of an annuity decides everything. It determines where your money goes, how returns are calculated, when payouts are adjusted, and which currency events shape your final outcome.

When you look at an annuity only at the surface level, you see a fixed rate or a promised payout. But when you look deeper, you see that some of those promises depend on markets you do not control.

Once you know the structure, you can decide whether the product supports your goals or limits your flexibility. This is how you keep your future runway strong instead of tied to forces outside your business.

How Mapping Out Currency Exposure Makes Your Plan Stronger

Currency exposure is not something you guess at. It is something you map. Most founders have never asked which currency their future payouts depend on, because most sales materials do not mention it.

But when you map this exposure, you learn whether your annuity is tied to stable markets or volatile ones. You learn whether your real income depends on political stability in another country.

You learn whether your future cash flow might float up or down based on events far away from your business. With this map, you can decide whether the risk aligns with your planning horizon.

This gives you the power to choose products that support your real needs instead of fighting against them.

Why Eliminating Unnecessary Conversions Protects Your Capital

Every conversion is a cost. If your annuity forces multiple conversions, your payout shrinks piece by piece. Founders need to understand how many times their money will switch currencies over the life of the contract.

Sometimes the number is shocking because the contract never says it directly. When you reduce the number of points where conversions happen, you keep more of your money.

This is not about getting rich. It is about avoiding friction. The less friction your money faces, the more of it stays available for growth, hiring, and product work.

How Matching Your Payout Currency to Your Spending Currency Creates Stability

One simple way to protect your annuity value is to match the currency of your business expenses with the currency of your payout.

If your business runs in dollars, and your annuity pays in a foreign currency before converting back, you carry unnecessary risk and unnecessary cost.

But if you choose a product that pays in the same currency you already use, your plan becomes cleaner. You remove conversion drag.

You remove unnecessary volatility. You remove guesswork. This simple match creates stability that supports your company rather than disrupts it.

How Tax Transparency Turns a Confusing Plan Into a Predictable One

Founders do not need to know every tax rule. They only need transparency. Tax transparency means knowing whether the annuity triggers foreign withholding, whether your home country taxes the full payout, and whether any credits apply.

When these answers are clear, you can calculate your true net return long before the first payout arrives. This clarity matters because founders often plan their financial future down to the quarter.

When you know your real after-tax income, you can design smoother hiring plans, smoother expansion plans, and smoother budgeting cycles. When taxes are unclear, everything becomes harder.

Why You Need to Understand Where Your Annuity Will Be Taxed

Cross-border annuities introduce something most founders never think about: tax location. Some countries tax based on residency. Some tax based on citizenship. Some tax based on the source of income.

The location of the tax authority decides how much money you actually receive. When you understand this location, you gain insight into the real weight of the tax system.

Without this understanding, you may assume your payout is larger than it is. This mismatch can lead to decisions that stretch your finances at the wrong time, which can hurt a growing company.

How Reviewing Treaty Protections Keeps You From Paying Twice

Tax treaties exist to prevent double taxation, but they do not always work cleanly. Some treaties protect certain types of income but not others. Some reduce withholding but do not eliminate it.

Some help you recover taxes later but require heavy paperwork. When you review these treaty protections early, you learn how much of your payout you actually retain.

You also learn whether the process for claiming credits is realistic for your situation. Founders who understand these protections avoid paying twice and avoid the frustration of navigating unexpected rules later.

How Predictable Cash Flow Protects Your Business From Disruption

Founders run their companies on timing. When money arrives late or arrives in smaller amounts, your operations feel it immediately. When you build your financial plan around an annuity, you want predictability.

Anything that makes the payout unpredictable—currency shifts, FX spreads, tax delays—weakens your plan. The more stable your income stream is, the more confidently you can make decisions.

When your cash flow is predictable, your team moves faster, your roadmap stays intact, and your company avoids unnecessary pauses.

How Building a Buffer Protects You From Timing Surprises

Even when you choose the cleanest annuity structure, timing surprises can happen. Building a buffer is not about pessimism. It is about protecting your momentum.

A buffer gives you the space to handle temporary delays without slowing down your product or your hiring. It keeps your plans intact even when the payout timeline shifts slightly.

This small adjustment in your planning approach protects your company from friction that could otherwise show up at the worst time.

How Choosing the Right Annuity Structure Creates Real Strategic Freedom

At the end of the day, the goal is simple. You want money that supports your business, not money that surprises you. You want an annuity that works with your financial strategy, not one that creates extra problems to solve.

When you choose the right structure—one with clear currency exposure, minimal conversions, transparent taxes, and predictable payout—you gain strategic freedom.

You get more control over the future of your company. You get smoother planning. You get stronger resilience. You protect not only your money but your momentum.

Wrapping It Up

Before any founder, engineer, or business owner commits money to an annuity, it helps to step back and look at what you now understand. Annuities can look smooth and steady on the surface, but the deeper mechanics tell a different story. Currency shifts, FX fees, and cross-border tax rules can reshape the real value of your investment in ways that feel invisible at first and very real later. These hidden forces do not care about your roadmap, your launch timeline, or your hiring cycle. They move on their own schedule, and they shape how much money actually reaches your business when you need it.